Use our credit report dispute letter template to contest inaccurate items on your credit report.

Updated November 14, 2023

Written by Sara Hostelley | Reviewed by Brooke Davis

A credit report dispute letter allows consumers to challenge inaccurate, incomplete, or outdated information on their credit reports. This document can allow you to correct any mistakes in your credit history, which can help you take charge of your credit rating and financial future.

A credit report dispute letter is a type of written communication you can send to the credit bureaus to contest any errors, discrepancies, or inaccuracies on your credit report. The letter will identify your disputed items, explain the reasons for the disputes with supporting facts, and request the credit bureau to correct the information.

Unfortunately, mistakes are more common than many people realize. Failure to address these issues can create long-term credit issues. If you wait to report an issue, you may lose the evidence to prove the inaccuracies.

The Fair Credit Reporting Act (15 U.S.C. §§ 1681-1681x) grants you the right to dispute any information you believe to be incorrect, outdated, or unfairly reported in a credit dispute letter. This document formally requests the credit bureaus to investigate the disputed items and correct any inaccuracies.

You can dispute credit report information like:

You may notice an incorrect account number on your credit report. For example, two numbers on your mortgage statement may be transposed, or your report may show an entirely incorrect account number. In any case, you can settle these details in a dispute letter.

Your report may show you failed to make a payment entirely or made a payment late. If you have the evidence to prove these claims false, you may consider writing a credit dispute letter.

Review your report and look for instances of duplicate accounts. If the same credit account appears multiple times, you can request the removal of the duplicates.

Depending on your jurisdiction, a debt may have a statute of limitations between three and six years [1] , meaning a debt collector can’t pursue payment. Dispute any negative items beyond the legally allowed reporting period.

If you suspect fraudulent accounts or identity theft, dispute the accounts immediately. Someone may have tried to open an account in your name, but you can challenge this issue easily with a credit dispute letter.

If you’re a victim of identity theft, you can use an affidavit of identity form to prove who you are.

Be sure to include the following elements in a credit dispute letter:

Write your personal information in your letter, like your full name and mailing address. Include the primary address identifier, city, state, and ZIP code. This way, the credit bureau to whom you’re sending the letter can easily identify you and investigate your claim.

Provide your dispute information. Specify which item you’re disputing. You may dispute multiple items if necessary, but ensure to identify which ones so the credit bureau doesn’t think you’re disputing something accurate.

Explain the reason for your dispute(s) and provide documentation to support your claim.

Circle or highlight the disputed items on your credit report and attach a copy to your letter. This way, the credit bureau can easily see what you’re challenging.

Disputing an item on your credit report involves a systematic process to increase your chances of success. These steps can help you challenge an item on your credit report:

Request a report from any of the three major credit bureaus: Equifax, Experian, and TransUnion. According to 15 U.S.C. § 1681j(a)(1)(A), you can receive one free report from each bureau annually, which you can obtain through AnnualCreditReport.com.

To obtain your credit report, you’ll provide the following information:

Thoroughly review each report for any discrepancies or errors. Pay close attention to personal information, account details, and payment history. Some of the most common errors include late payments, duplicate entries, and outdated information.

Gather all relevant materials that support your dispute. These materials may include account statements, receipts, correspondence with creditors, or other evidence proving the inaccuracy.

Compile the evidence into documents to easily submit them with your credit dispute claim and letter.

Use a credit dispute letter template to draft your correspondence. Be concise about the items you are disputing and the reasons for your dispute. Include the date, source, and type of the item. Specify whether you want the bureau to correct or remove the items. Make sure to enclose copies of the supporting documentation.

Refrain from including unnecessary or irrelevant information, which could slow the review process.

Send the letter via certified mail with a return receipt requested to ensure delivery confirmation and to create a paper trail of your dispute.

The credit bureaus typically have 30 days to investigate your dispute. They will communicate with the creditor or information provider to verify the accuracy of the information. The credit bureau must update your credit report if the information is inaccurate.

If you provided additional information after your original claim, the bureau to whom you submitted your claim will have 15 more days to review your disputed items.

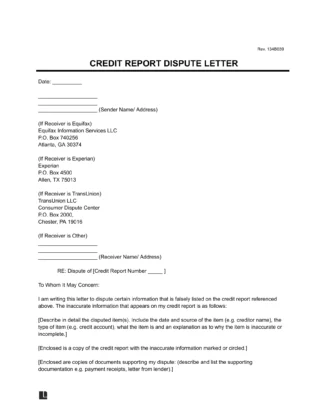

Review the contact information for the three major credit bureaus below:

Mail: TransUnion Consumer Solutions, P.O. Box 2000, Chester, PA 19016

Phone number: (800) 916-8800

Mail: Experian, P.O. Box 4500, Allen, TX 75013

Phone number: (888) 397-3742

Mail: Equifax Information Services, LLC, P.O. Box 740256, Atlanta, GA 30374

Phone number: (866) 349-5191

While the credit dispute letter is an effective method for disputing errors, you can initiate a claim by requesting a validation of debt.

15 U.S.C § 1692g(b) states a debtor can inquire about the origin of a debt by writing and submitting a debt validation letter to the original creditor. If the debtholder can’t obtain the original creditor’s name and address within 30 days, the debtor can have the debt taken off their credit report.

You may also choose to pursue the following routes:

If the debtholder validates the debt by writing back with the original creditor’s information, you can consider waiting six months to try sending another debt validation letter.

Companies often sell their debts, so the new debtholder may not respond to your letter. Without a timely response, you can have the debt taken off your credit report.

15 U.S. Code § 1681(a)(4) states all debts expire after they’ve been on an individual’s credit report for seven years. After this period, you may have to submit an additional claim since the debt won’t remove itself automatically.

Viewing a sample letter can help you confidently challenge erroneous information on your credit report. Download our free credit report dispute letter template as a PDF or Word file to have as a guide: